Option

Description

Up to Tax Month

Select the month that the Employer Payment Summary is being submitted for. This will default to the latest month in Payroll. If you pay HMRC quarterly rather than monthly (and the P32 Payment Frequency option on the Payroll - Utilities - Set Options form is set to 'Quarterly') then the quarter number is displayed in the list where appropriate.

Recovered amounts

Enter the recoverable amounts for Statutory Payments, National Insurance contributions (the figures that are displayed initially are taken from the updated figures on the Payroll - P32 Processing form but you can change them if required).

You need to enter CIS Deductions Suffered if necessary - this amount is not derived from the P32 Processing form.

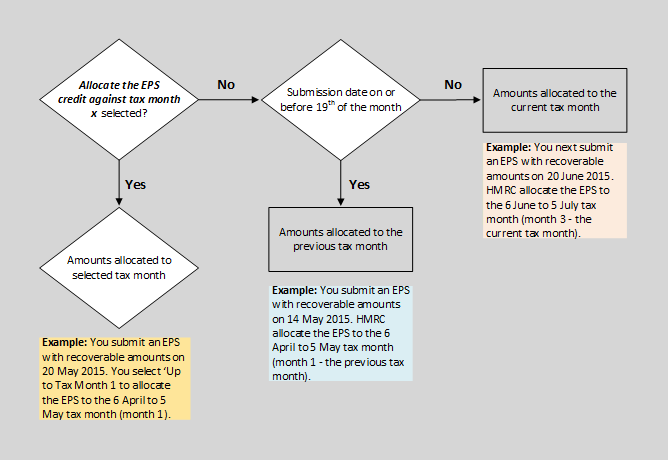

Allocate the EPS credit ... against tax month x

When this box is selected the recoverable amounts are allocated against the month in the Up to Tax Month box. When this box is cleared the tax month that the recoverable amounts are allocated to depends on the submission date.

This flowchart illustrates the tax month that recoverable amounts are allocated against, depending on whether this option is used or when the EPS is submitted.

Bank Account Details

Enter bank details to which refunds will be sent by HMRC if relevant. This information need only be provided once but can also be included each time an EPS is submitted.

2024/25 tax year

Employment Allowance: Employers can reduce their secondary Class 1 National Insurance Contributions (NICs) by up to £5,000.

Eligibility: Employers with a secondary Class 1 NICs liability of £100,000 or more in the wprior tax year are not eligible to claim the allowance.

2025/26 tax year and onwards

Employment Allowance Increase: From 1 April 2025, the Employment Allowance will increase to £10,500.

Eligibility Change: From 1 April 2025, the £100,000 eligibility threshold will be removed, meaning employers whose secondary Class 1 NICs liability was £100,000 or more in the prior tax year will be eligible to claim the allowance.

These changes are designed to provide more support to employers, especially larger ones, by increasing the allowance and removing the previous eligibility cap.

De-minimis State aid rules

Prior to the 2025/26 tax year, extra checks were required to ascertain a company’s eligibility for the Employment Allowance as it advantages some businesses over others, which potentially could distort competition and Trade within the European Union.

For the 2025/26 tax year, HMRC are responsible for ensuring compliance with the de-minimis state rules and advise that the State aid rules don’t apply option within the Employer Payment Summary is not selected.

From the 2026/27 tax year onwards, the State aid rules options have been removed from the Employer Payment Summary.

You should record the employment allowance that you claim on the

Payroll

- P32 Processing - Employment Allowance form. It will then

be deducted from the total amount shown to be paid to HMRC.

You should record the employment allowance that you claim on the

Payroll

- P32 Processing - Employment Allowance form. It will then

be deducted from the total amount shown to be paid to HMRC.

The Employer Payment Summary (EPS) is used to claim the Employment Allowance.

One of these options on the EPS screen in Payroll must be selected:

Can't claim

Stop claiming

Starting to claim or already claiming for the current tax year.

Before 2026/27 tax year

HMRC advise that the State aid rules don't apply option in the Employer Payment Summary should be selected.

2026/27 tax year onwards

The State aid rules options have been removed from the Employer Payment Summary.

Select one of the following options for the Employment Allowance.

Can't claim

Select this option to signify to HMRC that the Employment Allowance can't be claimed by the company.

Stop claiming

Select this option to signify to HMRC that the company was claiming the allowance but it will no longer be claimed because the business is no longer eligible. Stopping your claim means that no allowance is due, and you must pay all Class 1 NICs as a result.

Important:

1. Do not select ‘Stop claiming’ to indicate that you have claimed

the full allowance for the tax year.

2. Do not select ‘Stop claiming’ to indicate that you are no longer

employing anyone.

Starting to claim or already claiming

Select this option to indicate to HMRC that the Employment Allowance is being claimed for the current tax year.

Even if an EPS to HMRC has never been sent to HMRC other than

for the final tax month in a tax year, one must be sent to indicate

the intention to claim the allowance. Otherwise, HMRC will assume

the employer has underpaid their NICs.

State aid rules don't apply

Select if State aid rules don't apply to the business.